Working with Kiavi

The Complete Guide to DSCR Rental Loans

DSCR loans are a popular financing option for real estate investors because they qualify based on a property's rental income, not the borrower's W-2. Also referred to as investment property loans, non-QM loans, and rental loans, DSCR loans give investors a path to long-term rental financing with fewer traditional barriers.

What is Debt Service Coverage Ratio (DSCR)?

Before learning the ins and outs of a rental property loan, it's beneficial to understand the calculation and purpose of the debt service coverage ratio. Lenders use this ratio to determine if you have sufficient funds to repay your debt. The lender will use this information to decide how much money to lend when requesting a loan or refinancing an existing one.

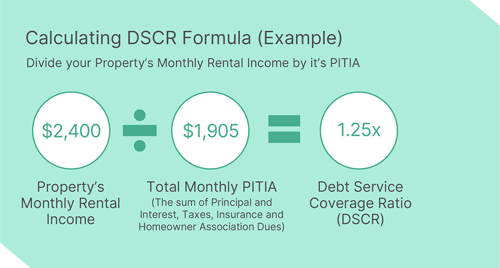

DSCR is the ratio of income generated for every $1 owed to the lender. The higher the ratio is, the more net operating income is available to service the debt. For example, a 1.25x DSCR reflects that the asset generates $1.25 for every $1 owed.

Put simply, the DSCR looks at all the monthly debt payments associated with the property, including loan payments, and compares them to the property's monthly revenue. The lower the DSCR, the greater the risk you may have to go out of pocket to pay the loan should the property sit vacant, or the operating expenses turn out to be higher than expected.

DSCR Calculation for a Single-family Rental Property

A simple way to calculate your DSCR and measure your cash flow is to divide the monthly rent by the PITIA (principal, taxes, interest, insurance, and association dues). The resulting ratio lends insight into your ability to pay back the loan based on your property's monthly rental income.

Note: Each lender will likely have a slightly different method of calculating DSCR, so it's best to inquire about exact numbers with your lender.

Qualifying for a DSCR Rental Loan

When qualifying for a DSCR loan, the lender considers several factors, including the borrower's credit score, available down payment, and the debt-service coverage ratio of the property. Typically, the credit score dictates the interest rate, and leverage is determined by credit score and DSCR combined. DSCR measures the asset's ability to pay the property's mortgage and expenses—so the higher it is, the more leverage the investor can get, which means less out-of-pocket cash at closing.

If you're looking to obtain a DSCR loan, it's best to be aware of these basic requirements:

- Minimum Credit Score: Most DSCR lenders, including Kiavi, require a minimum FICO score to pre-qualify. Your credit score may also affect your interest rate and available leverage.

- Minimum Down Payment or Equity: Maximum LTV varies by lender, property type, and DSCR. The remainder is your down payment. See current terms at kiavi.com/loans/rental for Kiavi's requirements.

- Minimum Property Value: Most DSCR lenders have a minimum property value requirement. Reach out to your Kiavi representative for specifics.

Reach out to your dedicated Kiavi representative to learn more about Kiavi's requirements.

What is a Good DSCR?

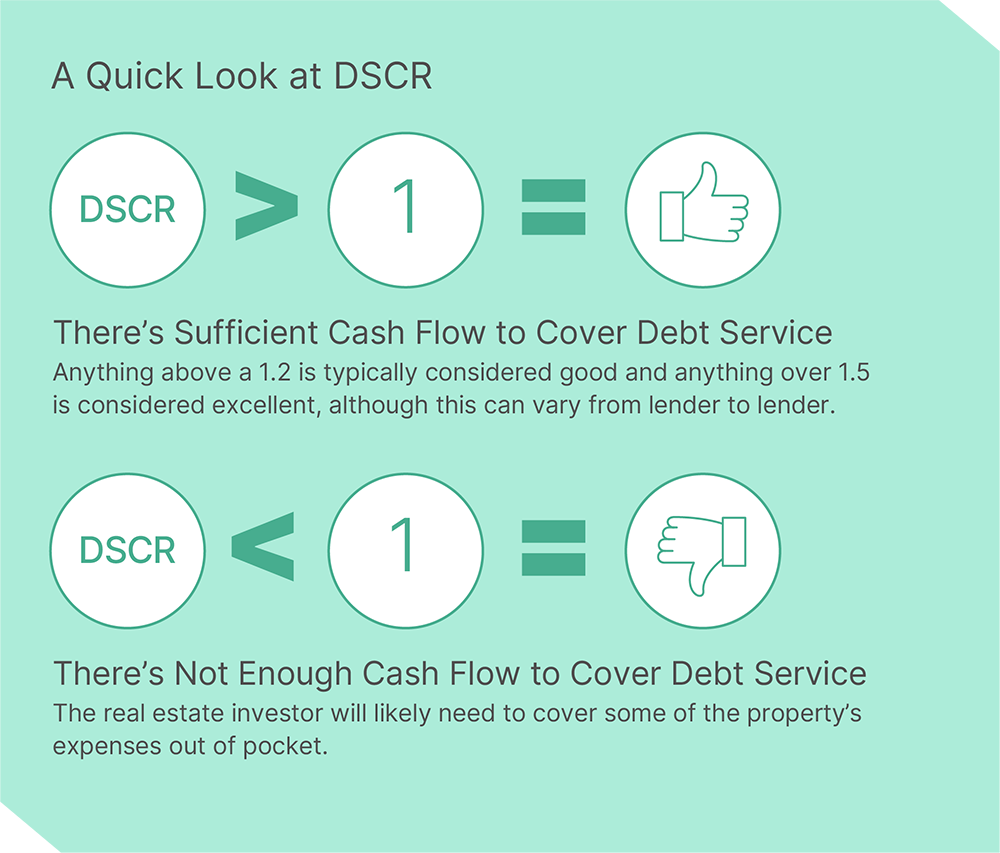

Lenders often consider a "good" DSCR to be 1.25 or higher because it indicates the property generates 25% more income than its debt obligations, which may provide a positive cash flow buffer even if expenses fluctuate or the property experiences temporary vacancy.

The closer you are to breaking even, the less cash flow you'll have to work with, making the investment more sensitive to vacancies or unexpected costs. If your DSCR on a particular deal is below 1.0, your rental income is less than your total debt service, which means the property may not cover its own loan payments each month. Running the numbers carefully before moving forward is always worth the time.

Why Do Real Estate Investors Use DSCR Loans?

You can borrow as an entity or LLC

Many experienced real estate investors prefer to borrow through an LLC or corporation, and several private money lenders require you to have an entity. Doing so adds an extra layer of protection to your personal assets should anything go wrong with the investment property. Traditional mortgage loans, however, can only be obtained in an individual's name.

You have an increased ability to scale your rental portfolio

Even if you have enough personal income to support multiple mortgaged rentals, traditional lenders have maximum limits on the number of mortgages they allow a borrower to have at one time. This is not the case with most DSCR lenders. Instead, they use common sense when evaluating your maximum credit exposure.

Refinancing options are available

Most DSCR programs also provide rate, duration, and cash-out refinancing options. In certain scenarios, a DSCR loan may permit you to withdraw more money from an investment property than you would be able to with a conventional loan, allowing you to use the equity to purchase your next property.

Less documentation is required

Chances are you've experienced the rigmarole of applying for a traditional mortgage. You have to jump through hoops to gather paycheck stubs, bank statements, tax documentation and more as the underwriters dive deep into your personal financial documents and history.

This process can be time-consuming, tedious and frustrating. This is not the case when you work with a DSCR lender. Because they're focused on the investment property's value and expected cash flow, they won't typically ask you for documentation to verify your employment, income or assets.

Pros

Increased Accessibility

Because lenders don't consider your personal income, DSCR loans are much more accessible —even if you don't have a large amount of liquid capital.

Greater Investment Protection

Since DSCR loans allow you to borrow on an LLC or business entity, you can further protect your personal assets and other investments.

Quicker Closings

Without income verification requirements, the application process is more straightforward and may allow for faster closings than a conventional mortgage.

Finance Multiple Properties at Once

With a traditional mortgage, you often can only commit to one property at a time. With a DSCR loan, you can take out different loans for different properties simultaneously up to your exposure limit. Plus, you can refinance with a cash-out option to purchase your next property.

Cons

Specific Loan Qualifications

Qualifications are weighted toward a good DSCR ratio to get the highest leverage and best rates and terms.

Higher Interest Rates and Down Payment

Typically, interest rates are higher, and a larger down payment is required on a DSCR loan than a traditional mortgage.

Are you experienced working with real estate investors?

When searching for a DSCR lender who is knowledgeable in working with investors, it is beneficial to investigate certain characteristics that could indicate their level of experience. These indicators can help to determine how well the lender is prepared to fulfill your financing requirements as a real estate investor.

- How long the lender has been in business

- How many of the lender's projects have successful exits

- How many projects the lender has funded

- The dollar amount of loans funded

- If they specialize in DSCR or rental loans

- How well they know local rental market trends

What are your fees?

Before you commit to any loan, you must know the total financing costs to ensure you don't incur any unexpected charges at the end. Typically, there will be a processing fee and some type of administrative payment, such as an underwriting or service fee. A trustworthy lender will be transparent about any additional expenses or hidden fees.

What are your eligible property types?

Different lenders offer varying types of loans. For instance, some may have DSCR loan programs, particularly for vacation rental purposes, while others may not. Additionally, there are variations regarding warrantable or non-warrantable condos and multiplex properties.

How do you calculate rent in the DSCR?

The rent figure a lender uses in the DSCR calculation can affect how much you're able to borrow. Some lenders use only the lower of appraised market rent or your signed lease rent. Kiavi uses the lower of 110% of appraised market rent or your signed lease rent when the lease is valid, which may support a stronger loan amount on well-performing properties. Ask your lender how they treat rent in the calculation before you apply.

Can I compare loan structures before I commit?

The ability to compare loan scenarios before submitting your application can make a meaningful difference in your deal analysis. Kiavi's platform lets you adjust LTV, loan amount, and prepayment terms side by side and see how each combination affects your rate and monthly payment. Not all lenders offer this level of visibility before the application stage.

What does my monthly payment actually include?

A DSCR loan payment typically includes principal, interest, taxes, and insurance (PITI). Ask your lender whether they show you an estimated PITI amount and implied monthly cash flow before closing, so you can evaluate the deal on accurate numbers. Kiavi's loan terms display both, with taxes and insurance moving from estimated to finalized as your loan is underwritten.

Ready to Apply for a DSCR Rental Loan?

Kiavi's DSCR rental loan platform gives you transparent terms, a clear view of your loan options, and real support from a team that understands investor financing. See your rate online and explore your options before you commit.

You are leaving kiavi.com. Do you want to continue?